Joint Economic Forecast Autumn Report 2024: German Economy in Transition ‒ Weak Momentum, Low Potential Growth

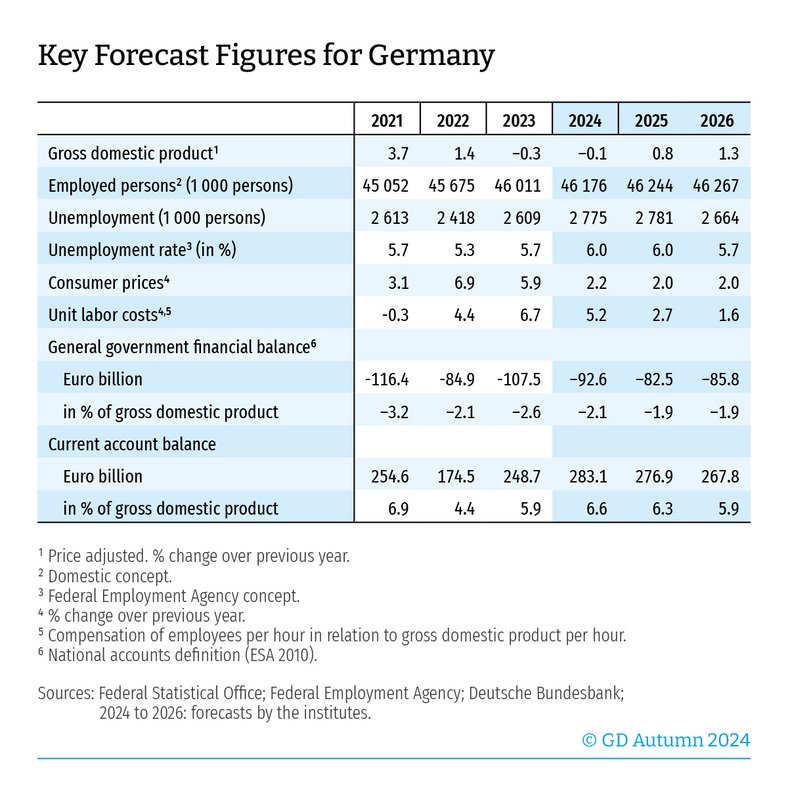

The German economy has been stagnating for more than two years. A slow recovery is likely to set in next year, but economic growth will not return to its pre-coronavirus trend for the foreseeable future. The overlapping effects of structural change and the economic downturn are particularly evident in the manufacturing sector. Capital goods manufacturers and energy-intensive industries are particularly affected. Their competitiveness is suffering from higher energy costs and increasing competition from high-quality industrial goods from China, which are displacing German exports on world markets. In terms of the economy, the manufacturing industry is also struggling with the weakening of the global industrial sector and the associated lack of new orders. This is mitigated by the strong increase in gross value added in select areas of the service sector, particularly those dominated by the state, such as education and healthcare.

The Joint Economic Forecast Project Group considers the continuing weakness in investment to be symptomatic of the problems in the manufacturing sector. The persistently high interest rate level alongside the elevated economic and geopolitical uncertainty are likely to have weighed heavily on the investment activities of companies and the propensity of private households to make purchases. Private households are increasingly saving their money instead of spending it on new residential property or consumer goods.

According to the report, the structural adjustment processes are likely to continue and the economic brakes will only be gradually released. The tentative recovery is driven by a revival in private consumption, which will be supported by strong growth in real disposable incomes. The upturn in key sales markets, such as neighboring European countries, will support German foreign trade. Together with more favorable financing conditions, this will benefit investment in fixed assets.

The economic standstill is now showing clearer signs on the labor market with slightly increased unemployment. It is only in the course of 2025, when economic activity gradually recovers, that unemployment is likely to fall again.

In August, the inflation rate fell to its lowest level in more than three years and is expected to remain close to the European Central Bank's (ECB) inflation target of 2 percent through 2026.

The full-length version of the report is available at www.gemeinschaftsdiagnose.de/category/gutachten/.

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the Federal Ministry for Economic Affairs and Climate Action. The following institutes participated in the autumn report 2024:

- German Institute for Economic Research (DIW Berlin)

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich in cooperation with the Austrian Institute of Economic Research (WIFO) Vienna

- Kiel Institute for the World Economy (IfW Kiel)

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna

Scientific contacts

Dr Geraldine Dany-Knedlik

German Institute for Economic Research (DIW Berlin)

Tel +49 30 89789 486

Professor Dr Oliver Holtemöller

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

Tel +49 345 7753 800

Oliver.Holtemoeller@iwh-halle.de

Professor Dr Timo Wollmershäuser

ifo Institute – Leibniz Institute for Economic Research at the University of Munich

Tel +49 89 9224 1406

Professor Dr Stefan Kooths

Kiel Institute for the World Economy (IfW Kiel)

Tel +49 431 8814 579 oder +49 30 2067 9664

Professor Dr Torsten Schmidt

RWI – Leibniz Institute for Economic Research

Tel +49 201 8149 287