Joint Economic Forecast Autumn Report 2025: Fiscal stimulus masks structural weakness

The German government is using expanded debt rules to strengthen defense capabilities and invest in infrastructure and climate protection. This will provide stimulus in the coming years, but with limitations: First, funds for construction and defense projects, for example, are being disbursed more slowly than budgeted due to long planning and procurement times. Second, loans are also being used to avoid consolidation that is actually due. Third, despite the deferred funds from the expanded borrowing options, there will be a considerable need for consolidation in 2027.

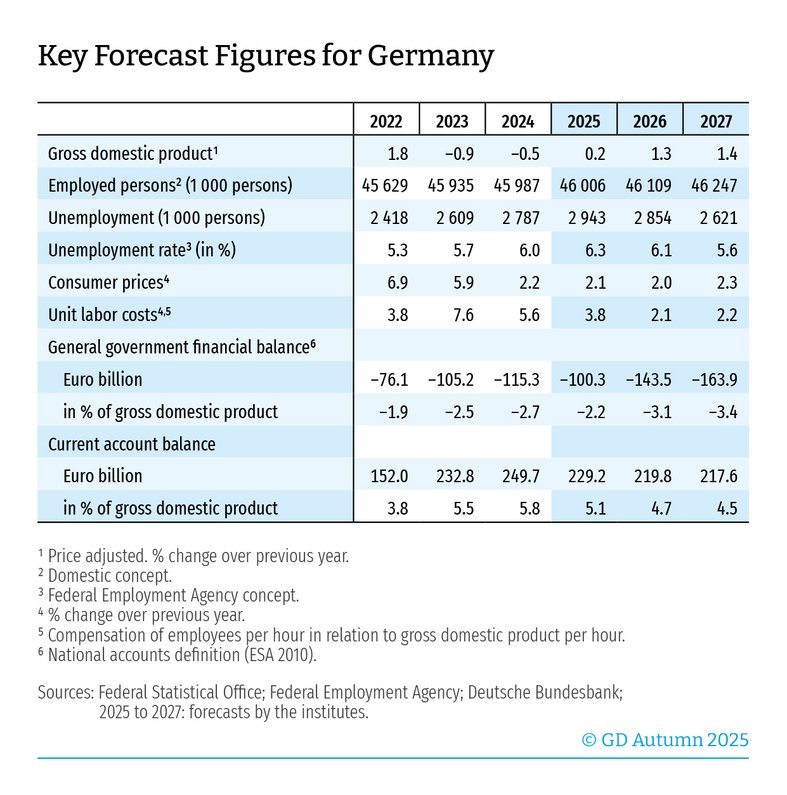

Nevertheless, the domestic economy is picking up speed noticeably, but the structural problems are only being concealed: fundamental reforms to strengthen the economy are not being implemented. The outlook is deteriorating, which is also reflected in the expected decline in growth rates of production potential. High energy and unit labor costs by international standards, a shortage of skilled workers, and a further decline in competitiveness continue to dampen long-term growth prospects.

While the service sectors, particularly in the public sector, will grow strongly over the next two years, the recovery in the manufacturing sector is likely to be modest. Foreign demand for German goods is weakening in particular due to declining competitiveness and higher tariffs. As a result, strong growth in exports will not be a driving force in the coming upturn. Supported by expansionary fiscal policy, the recovery is concentrated on the domestic economy.

The economic upturn is also likely to bring about a noticeable improvement in the labor market. Together with rising real disposable incomes, this will boost private consumption and thus consumer-related services. Consumer prices are expected to rise by a good two percent during the forecast period.

Overall, economic development in Germany is exposed to considerable risks: the trade dispute between the US and the EU has great potential for escalation, especially if EU commitments cannot be met. In addition, the macroeconomic impact of expansionary fiscal policy is difficult to assess and depends heavily on the specific design of the policy.

Germany is at an economic turning point, as growth prospects are deteriorating rapidly. To provide guidance, the institutes present a twelve-point economic policy compass. If these reforms were implemented promptly, this would not only strengthen the long-term growth potential of the German economy but also stimulate it in the short term.

The full report is available at www.gemeinschaftsdiagnose.de/category/gutachten/.

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the Federal Ministry for Economic Affairs and Energy. The following institutes participated in the autumn report 2025:

- German Institute for Economic Research (DIW Berlin)

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich in cooperation with the Austrian Institute of Economic Research (WIFO) Vienna

- Kiel Institute for the World Economy

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna

Scientific contacts

Professor Dr Torsten Schmidt

RWI – Leibniz Institute for Economic Research

Tel +49 201 8149 287

Dr Geraldine Dany-Knedlik

German Institute for Economic Research (DIW Berlin)

Tel +49 30 89789 486

Professor Dr Stefan Kooths

Kiel Institute for the World Economy

Tel +49 431 8814 579 or +49 30 2067 9664

Professor Dr Timo Wollmershäuser

ifo Institute – Leibniz Institute for Economic Research at the University of Munich

Tel +49 89 9224 1406

Professor Dr Oliver Holtemöller

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

Tel +49 345 7753 800